Strategy consulting in an age of crisis

In terms of the professional services market, strategy consulting is both the first casualty of any crisis and one of the most important lead-indicators of recovery. But what happens in an environment of multiple, overlapping crises?

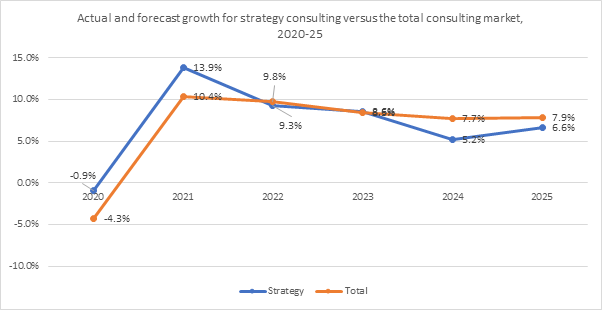

True to form, client demand for strategy consulting—which, for these purposes, we’ll define here as the provision of advice around the objectives and overall direction of an organisation, which typically combines extensive analysis with complex, board-level debate—collapsed in April 2020. Compared to conventional financial crises, the situation was unprecedented: Most organisations had a vast array of urgent operational issues to resolve. But, by the summer, attention had started to switch to speculating about what the post-COVID world would look like and there was a recognition—which gained momentum through the autumn and on into 2021—that future success would depend on speed and adaptability. As a result, the strategy consulting market grew by an estimated 14% overall in 2021, four points higher than the market average. But, going forwards, we think growth in strategy consulting is more likely to be in line with, or slightly below, that average.

We see three reasons why demand for strategy consulting is unlikely to continue growing at its current level.

First is the definition of strategy consulting itself. Over the last decade, demand for work labelled as “strategy” may appear to have grown, but the type of work carried out in practice has changed. While traditional corporate strategy assignments do still happen, much strategy work has been subsumed into transformation, driven by the potential of new technologies to change business models and to disrupt entire industries. Even five years ago, a major strategy firm we interviewed said that half of its business could have been more accurately described as digital transformation. Although this shift is often characterised as paving the way for strategy firms to move downstream into more operational work, it would perhaps be more accurate to say that operational work moved upstream and, when combined with technology change, became an integral part of strategy.

The second reason—and it’s a direct consequence of the first—is that more consulting firms claimed they did strategy work. The economic case to do so was compelling: The combined market for strategy and digital technology enablement was immense. Moreover, strategy was seen as an agenda-setting activity that would inevitably lead to more work in other areas. This was overly optimistic in our view. Although some strategy work does result in programme management-style work, most clients see strategy as a standalone activity. Clients also think that firms that are good at formulating a strategy aren’t automatically good at implementing it, and they baulk at the idea of paying strategy prices for non-strategy work and/or non-strategy firms.

Both of these reasons pale into comparison with the third, however. The pandemic may be (almost, hopefully) over, but—in clients’ eyes—it is being superseded by other crises. First is climate change and now, especially where Europe is concerned, there’s the Russia-Ukraine war, the economic sanctions on Russia, and the long-term implications for access to fuel and raw materials, the location of production facilities, supply chains, and inflation. Will strategy be the first casualty of these crises too?

At first sight, the Russia-Ukraine war appears to pose the biggest threat. Once again, there’s huge uncertainty and disruption, which could put investment decisions on hold and herald a return to short-termism. But, as we noted in our last market update, the war has already produced a surge in demand for scenario planning, especially among multinationals based in Europe. Although the purpose of such work is to explore different possibilities, the fact that clients think it’s possible to construct and analyse a range of different scenarios suggests that they’re not paralysed by uncertainty in the way they were in the second quarter of 2020. This in turn suggests that any negative impact on the demand for strategy work will be short-lived.

One might be tempted to think that, after decades of scientific research on climate change, there’s no shortage of data about this crisis, providing strategy firms with an opportunity to explore and plan for multiple scenarios here, too. However, our research suggests that this isn’t the case in practice. On the one hand, there isn’t enough data about reporting requirements—they’re not yet agreed on, so planning ends up being hypothetical in the extreme. On the other hand, there’s too much data coming from a wide variety of sources—but it’s not clear to clients which is material to make change happen, and strategy consultants are no better placed than anyone else to advise clients what they should be focusing on. Climate change may therefore turn out to be less of an opportunity for strategy firms than they might have anticipated.

All of the above boils down to one, key point:. Strategy consulting thrives at the end of a crisis, when clients start to plan for the future, not at the beginning of one. In an environment in which organisations face what they consider to be wave after wave of crises, clients will become less likely to reach a point of sufficient stability to make longer-term decisions. There’s a danger that strategic decisions, like strategy consulting, will be something for the future, but less relevant in the present.