Data & analytics: The key to successfully responding to economic uncertainty?

For clients weighing up how to deal with high inflation and fuel costs, the threat of recession, and the other difficulties currently facing businesses, their most important is information.

That was the lesson of the pandemic, and it remains just as true today, despite significant investment in data & analytics over the last two years. This will translate into higher-than-average growth for professional services firms—but it’s not without its own challenges.

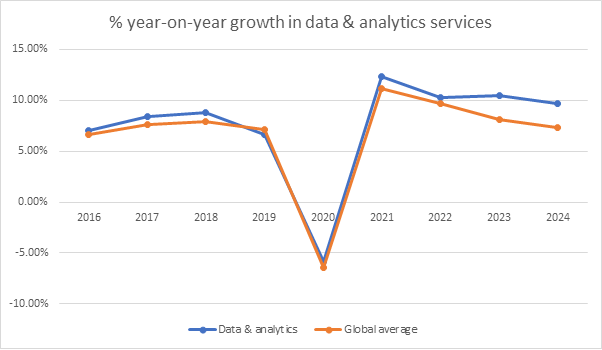

In 2016, the global market for data & analytics services was worth just under $40bn, equivalent to around 5% of the professional services industry. But by 2019, growth in this market had slowed to slightly below the market average as clients–realising that these skills were likely to be core to their organisations–began to reduce their reliance on external support. However, data we gathered in 2020 suggested that lack of up-to-date, robust, and timely data was the biggest practical issue organisations faced. Consumption and other models, honed over years, could no longer be relied on. It’s a picture that’s reinforced when we look at our market data. As a consequence, demand for data & analytics contracted less than the rest of the market and has recovered more quickly. We’re also forecasting demand for data & analytics work to stay relatively high, even as the market average returns to more normal levels by 2024. Between 2020 and 2024, we expect the size of the data & analytics market to have increased by half, to $71bn.

This forecast is based on data from clients, 54% of whom say that their data & analytics functions will be one of the three areas within their organisations where they’ll be making the greatest investment over the course of the next 18 months. In some geographies (France, China, the Gulf region) and some sectors (energy, resources & utilities, technology, media & telecoms) the proportion is even higher. More specifically, with rising fuel and other costs threatening individuals’ discretionary purchases, clients are investing to ensure they have better, more up-to-date information on consumer behaviour, and on being able to forecast demand more accurately, both at the overall level and for specific products and services.

However, clients remain keen to minimise their use of external support. One in five organisations is investing now in order to improve their in-house analytics capabilities for the future. Almost as many are trying to automate more, including some of their analysis. This means that, while there’s good news for professional services firms in that a third of clients say they’re likely to use significantly more external support in the data & analytics area over the course of the next 12 months, almost one in six organisations say it’s the area they’re least likely to look for help in because they’ve already been building up their own capabilities.

The data & analytics opportunity is therefore something of a double-edged sword. For professional services firms there’s the tantalising prospect of higher-than-average growth but tinged with the threat that clients may poach the best people. It’s tempting to say that suppliers’ advantage will lie in their deep expertise, but that competitive edge will be hard to maintain at a time when client organisations are willing to pay top-dollar for analytics skillsets. Having alliances with specialist analytics firms and software companies will be critical, as it won’t make sense for clients to try and replicate the scale and depth of such relationships. But the key will probably lie in professional services firms’ ability to create proprietary software tools, which help to differentiate them not only from other firms, but also from clients’ in-house resources.

Although such tools will require time and investment, the data & analytics market is likely to remain strong while economic uncertainty remains high and consumer behaviour remains unpredictable—which probably means for quite a long time.