US clients are more concerned about the macroeconomic situation, but demand for external support remains strong

Three months on from our last quarterly survey of client sentiment, and most senior executives in the US are determined to hold onto their ambitious, post-pandemic corporate goals, but need help doing so.

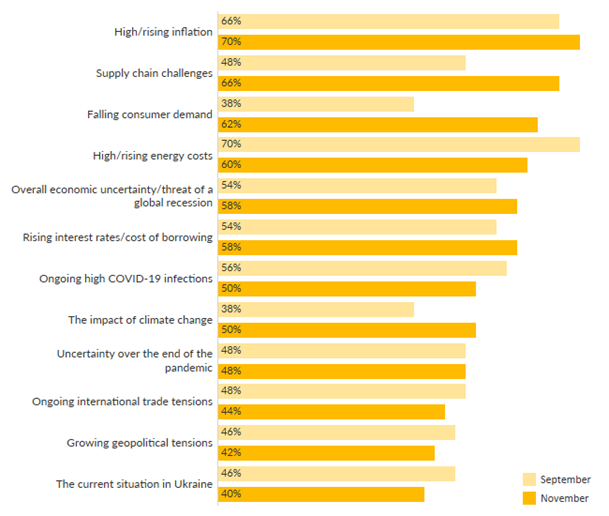

There’s no question: US clients are more worried than ever by the global trends they see. High/rising inflation continues to top the bill, with the proportion of clients who say that their organisation has already been negatively impacted by this or is likely to be in the next six months increasing from 66% two months ago, to 70% now. But the biggest jumps in anxiety levels were in 62% of clients who said they’re concerned about falling consumer demand (a 24-point increase) and the 66% who are worried about supply-chain challenges (up by 18 points on the previous research).

Percentage of US clients saying their organisation has been negatively impacted by…

Consequently, confidence is falling. Ninety-six percent of US clients say they’re less confident about the economic situation than they were two months ago. This has direct implications for their ability to invest: Just 6% of clients say that they expect to maintain their current investment plans.

But—and here is the good news for professional services firms—a deteriorating situation is driving US clients to use more external help, not less: Ninety-four percent say they expect to spend more on consulting and other professional services in response to the array of crises they’re facing.

The situation seems implausible, but it’s borne out by many conversations we’ve had with senior leaders in consulting firms over the last 2-3 weeks. Although there are specific areas where demand has taken a hit (transaction support for PE firms is widely seen to have dropped off a cliff, for example, when it was running at around 25% growth in the first half of 2022), overall growth remains exceptionally strong. Despite some softening of operational indicators (e.g., utilisation) in the last month, many pipelines stand at impressively high levels.

Despite this, we think US firms should remain cautious, for four reasons. First, there’s consumer spending. This is one of the key indicators that is likely to herald a change in client behaviour, as—our research shows—it results in cutting almost all types of external support, while most other economic shifts produce cuts to some services but increased, offsetting demand in others. In this latest survey the proportion of clients who say they’re concerned about falling sales has risen from 56% to 62%, making it the third biggest area of concern. Second, the labour market is easing—a point we made in our last update. While most executives say their teams are still overworked and stressed, the proportion who describe themselves as being very short-staffed is falling in some sectors, such as financial services. Any increase in capacity on the client side will reduce demand for staff augmentation—however, the shifts here will be gradual and only felt over several months. Third, there’s a factor which we suspect but cannot prove from our numbers, that clients are being overly optimistic about the ability of their organisation to withstand negative macroeconomic trends. Senior executives in particular, whose careers depend on their ability to deliver their ambitious corporate goals, may be living in hope. Finally, we have the response of suppliers. The third quarter of 2020 demonstrated that people businesses can be just as hard to change as ones based around large, physical assets. The lockdown paralysis of Q2 2022, in which clients tried to do most work themselves, quickly gave way to a recognition that organisations lacked the capabilities needed to make necessary change happen quickly. But consulting firms, caught by surprise, took around three months to create offerings that resonated with clients’ new needs.

The takeaway from all this is that two things matter in the current market: Consulting firms’ ability to anticipate, to see which way the wind is blowing ahead of their immediate competitors—and the speed and success with which they can adapt to meet potentially seismic changes in clients’ needs. Professional services firms love nothing more than a complex methodology, honed over years, but that would require the one thing clients don’t have in the current environment: Time.