Investment in transformation remains strong, but will professional firms be able to leverage this?

For the last two updates, we’ve focused on a subtle shift taking place in the consulting and wider professional services market that’s likely to soften demand in the second half of the year.

Evidence from the supply side suggests that the proportion of firms whose quarter-on-quarter revenues increased in Q2 2022 is somewhat lower than in the first quarter of the year; the percentage of clients who say they’ll spend more on consulting services in the next 12 months, compared to the last, has fallen slightly overall—and more substantially in key markets, notably the US.

But this shouldn’t obscure the fact that clients are still planning significant investments—the challenge is how to ensure that clients turn to professional services firms for help, rather than trying to do the work themselves.

At a point of economic uncertainty many client organisations trim back their use of external help: As one client, interviewed in the first few weeks of the global financial crisis put it, “We’ve had to change our approach to cost-cutting. It used to be that we cut biscuits in meetings, travel, and consulting budgets—in that order. But now we cut the consulting budgets first.” Size matters. Consulting budgets were prime targets because they often run into millions of dollars. However, post-pandemic size matters in a different way. Back in the early summer of 2020, organisations stopped large-scale transformation programmes only to subsequently re-start them, because many of the actions they needed to take depend on fundamental change. Smaller consulting projects were more disposable.

Learning that lesson from the pandemic, organisations may be becoming slightly more cautious about small and mid-sized projects, but are reluctant to cancel large ones, without which they might compromise both their immediate response and their long-term resilience. On average, 56% of client organisations we’ve surveyed over the last six months say that they’ll be making a substantial investment in digital transformation, 45% say they’ll be investing in responding to climate change and other sustainability-related issues, and just over 40% that they’ll be putting money into workforce and organisational change.

All of that bodes well, but it won’t automatically translate into fees to professional services firms.

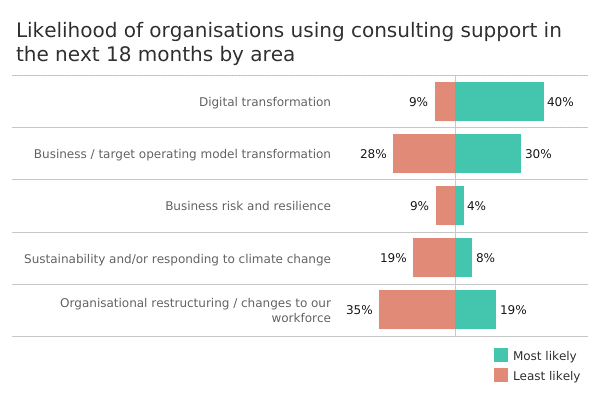

The chart below shows where clients say they’re “most” and “least” likely to use consulting support in the next 18 months—and it’s important to note that, when clients say something is an area where they’re least likely to use consulting help, that’s largely because they’re planning to do the work themselves.

This chart therefore tells us several things. First, digital transformation is the standout opportunity for external suppliers, irrespective of a looming recession, with 40% of clients saying they’ll be looking for consulting support, compared to just 9% indicating a preference to do the work in-house. By contrast, where support is needed for business model transformation, the proportion of clients planning to do the work themselves almost balances out those who plan to outsource. In the other three areas more clients expect to do the work themselves than bring in external help—something that’s especially marked in the organisational restructuring/workforce change space that around 40% of clients say they’ll be making a significant investment in.

What we infer from this is that consulting and other professional services firms should be reassured that planned investment levels are holding up reasonably well. But they should also be concerned that clients may expect to make more use of internal resources over external ones.