Some early insights into the Russian invasion’s impact on professional services

Our last update hypothesised that clients, having learned important lessons at the start of the pandemic, would be very quick to start evaluating their priorities in light of the Russia-Ukraine conflict and the economic sanctions that have accompanied it—and that would have an impact on the type of support they need from professional services firms. Some details of this evolution are starting to become clear.

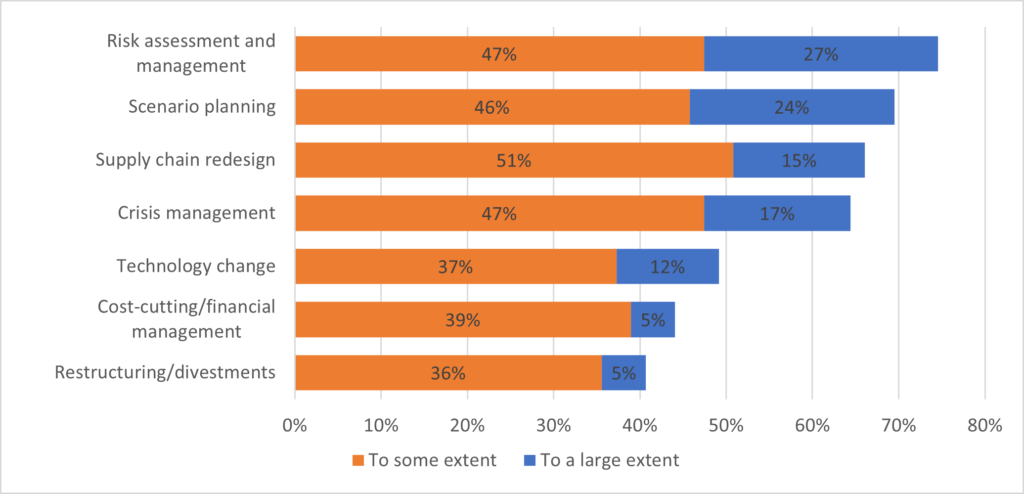

Based on a survey of consulting firms in March, there’s been a significant shift in the areas in which clients are seeking support. In the last quarter of 2021, digital transformation was the most sought-after capability, with 68% of consulting firms saying that this was one of the areas of highest demand. This was followed by workforce change and adaptation, productivity improvement, sustainability, and growth. In our latest survey, we asked about the services that have been most directly impacted as a result of the war—and the sense of priorities emerging from this is different. Consulting firms were most likely to point to risk management, followed by scenario planning, supply- chain design, and crisis management.

The details of this aren’t surprising: Given the situation, we would expect client organisations to redirect resources towards risk and crisis management at the expense of some areas of planned investment (e.g., in technology). The complex ramifications of sanctions are clearly behind the rising interest in supply-chain work; uncertainty is driving demand for scenario planning; and the interest in restructuring reflects the extent to which organisations with operations in Russia are being forced to reconfigure their business in response to economic sanctions.

What impact could this have on the overall size of the consulting market in 2022?

In our modelling, we’ve assumed that changing client needs will result in growth that is roughly twice the forecasted rate in the areas listed above (but higher for scenario planning as it’s starting from a much smaller base). In total, this could add almost US$4bn to the global market, equivalent to 2% of its total value, mostly from cybersecurity, operational risk, supply-chain work, and crisis management.

However, because the technology consulting market represents around 17% of the total market, even a small reduction in its growth rate has a substantial impact on the market as a whole. Based on client feedback so far, only part of the technology market will be impacted—most likely, some areas of investment in new technology as a part of broader digital transformation programmes.

For now, lower growth in technology revenues looks likely to be offset by the increases elsewhere, but our modelling does highlight the crucial issue for consulting firms. At least in the short term, the help clients are looking for because of sanctions appears to be specialised and relatively narrow in scope, whereas the technology projects that might be cancelled or curtailed as a result of sanctions are likely to be much larger in scale. It wouldn’t take a huge shift in the latter to change the picture of demand significantly. As consulting firms learned during the height of the pandemic, they will need to monitor these shifts and be prepared to rapidly adapt and reconfigure their services to respond effectively.