Technology services forecasts: Poised for above average growth

Our data continues to show that economic and political uncertainty will increase demand for external support—but that doesn’t mean growth will be evenly distributed.Our latest forecast (as at the end of Q1 2023), suggests that the global professional services market will grow by around 8% in 2023, in line with pre-pandemic averages but down on the 11%+ growth in 2021.

Economic and political uncertainty, while keeping business confidence low and reducing organisations’ capacity to invest, is leading to a greater reliance on external support. Why? Because clients want to get things done quickly and are chronically short of both capacity and specialist capabilities. In general, clients think that the polycrisis of rising costs, the Russia-Ukraine war, supply chain disruptions, etc., is bad but not deteriorating; they also think it’s going to be around for at least three years. All of which means that it makes sense to adapt to yet another new normal.

However, as we saw in 2020, what clients are prepared to spend money on is changing. Forty-four percent of clients say they’re most likely to use consulting around technology strategy, up from just 9% in 2022; 37% say they’re most likely to spend on technology implementation (we didn’t ask about this last year). Risk management, productivity improvement (including cost-cutting), and supply chain management are also more likely to be areas where clients spend more.

When clients say they’re least likely to use consulting support in any given area it doesn’t mean they’re not investing in it. Quite the reverse: It implies that they’re going to try and do the work themselves. We see evidence of this where data & analytics and cybersecurity are concerned with fewer clients compared to last year saying these will be areas where they’re least likely to look for external help. Overall, when we compare our 2023 data with that from 2022, the number of organisations that expect to use in-house teams is higher—just as it was at the height of the pandemic. Then—and now—clients tend to be optimistic about their organisational ability to get things done.

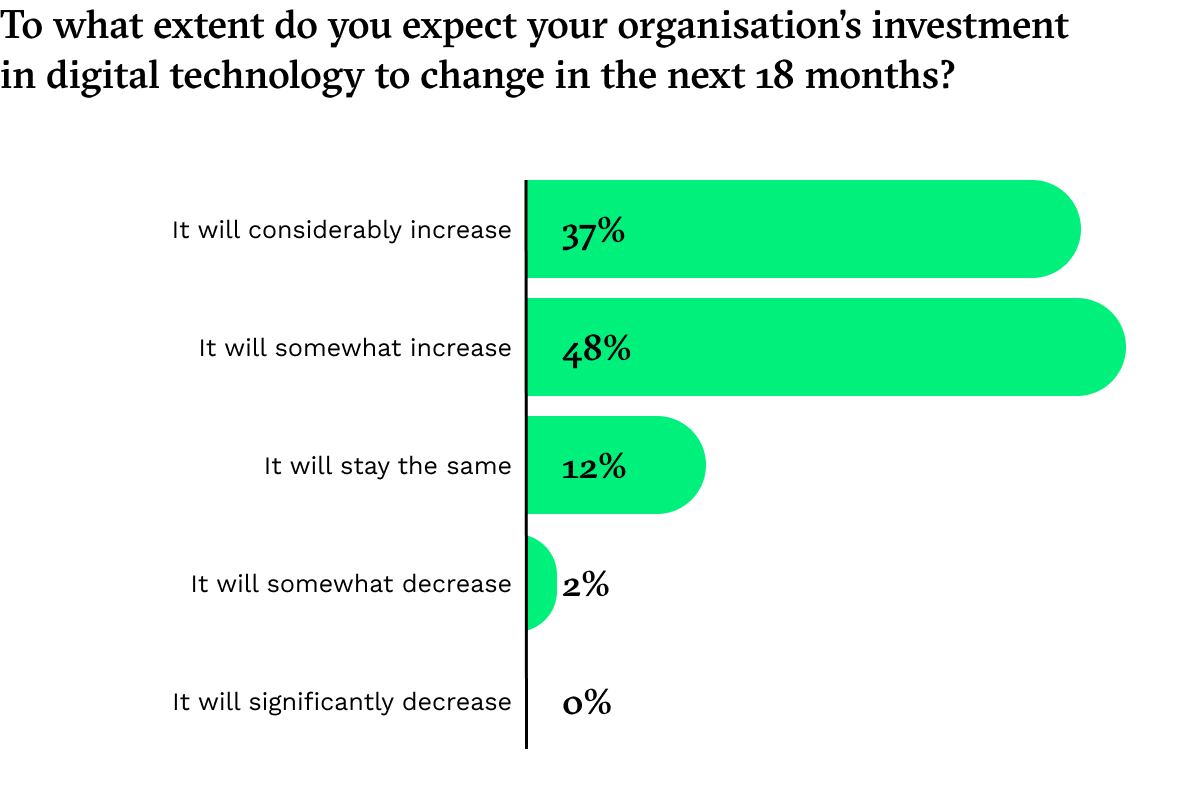

Technology is exempt from this optimism-to-disappointment cycle for the simple reason that clients know they won’t be able to recruit the right skills. Technology changes too quickly for them to keep up, and they can’t offer the high salaries and specialised career development opportunities a technology services firm can. A quarter of clients say that at least 80% of their workforces will need very different skills sets in the future. With 85% of organisations saying that they expect to invest more in digital technology in the next 18 months and 65% saying they need urgent upgrades to their technology to survive, they’re unlikely to keep pace with demand.

But increasing demand for technology services isn’t just because clients lack the right internal resources. Technology offers a potential solution to the three big concerns senior executives have now: It will help them reduce costs at a time when profits are falling; it will enable them to get more work done by fewer people; and it will speed up decision-making and execution across the organisation by providing access to more accurate and timely data.

How will that translate into market growth? Our latest modelling now has technology consulting growing at just under 10%, two points higher than the market as a whole. But growth in demand for large-scale digital transformation projects, in which technology is clearly a vital component, will be higher: Such projects may be somewhat reconfigured in the current environment, but we find very little sign that they’re being cancelled. Given the size of the technology consulting market—around $114bn in 2022—that will mean $11bn in new growth from last year to this. Add in systems integration and the market gets even bigger.

Small wonder, then, that all the firms we speak to are pivoting towards technology.