The impact of the professional services market pandemic recedes, but slowly

Two and a half years on, demand for professional services is still being shaped by COVID.

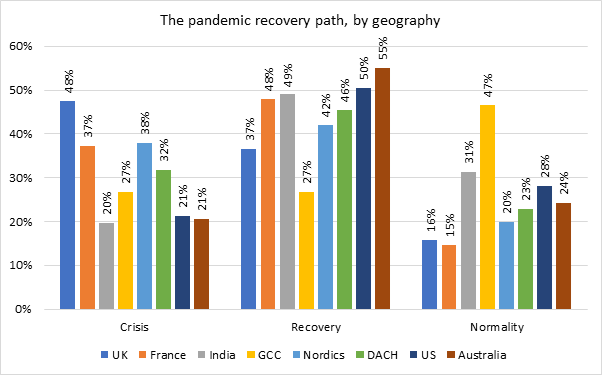

Over the last five months we’ve carried out research across a range of major markets, starting with the UK in early February, followed by France, India, the Gulf region (the GCC), the Nordics, and—more recently—in DACH (Germany, Switzerland, and Austria), the US, and Australia. Taken together, this research not only highlights important regional differences but also gives a sense of what the market is likely to look like going forwards.

We asked clients to describe the status of their organisation in relation to the pandemic. Were they still primarily focused on coping with its consequences? Had they started to plan for, and implement, the post-crisis future? Or had they emerged from the crisis and reached whatever passes for normality these days?

The UK, surveyed first, showed the slowest progress, with almost half of clients saying they continued to be in crisis mode, and only 16% in normality. While timing matters (the survey was carried out just after the Omicron peak), the data also showed that the slow pace of recovery in this market was as much to do with Brexit. Moreover, macroeconomic pessimism wasn’t stopping UK clients from bringing in external support: If anything, it appeared to make them more determined to find new ways to grow. The French market, surveyed a few weeks later and not suffering the same Brexit-related consequences, was more upbeat. Although 37% of clients said that they were still mired in the crisis, a higher proportion (48%) were in recovery. However, the proportion in normality was similar to that of the UK, suggesting that clients in France were more likely to stay longer in recovery, thinking longer and harder about the future.

Our next two markets—India and the GCC—were different. Both had a lower proportion of client organisations in crisis (20% and 27% respectively), and a much higher proportion in normality (31% and 47%). By contrast, in Europe, the Nordics and DACH markets, surveyed slightly later, were less positive than these non-European markets but slightly more positive than the UK and France had been a couple of months earlier. The US and Australia, surveyed only last month, are more positive again, though not yet reaching the heights of India and the GCC. Twenty-eight percent of US clients said that things were normal, and 24% of those in Australia did.

We would therefore hypothesise that clients in Europe are taking longer to reach normality, but that there has still been discernible improvement since the start of the year. And that’s despite the impact the Russia-Ukraine war is having—around 8% of DACH clients say that it’s having a significantly negative impact on their business, and a further 27% say the impact has been somewhat negative. The Gulf region bounced back strongly last year and is now being further fuelled by high energy prices. India is going through an extraordinarily fast digital transformation. The US and Australia are both important markets from a size perspective, collectively forecast to account for around 44% of the global professional services market this year. That only around a fifth of clients in these markets are still in crisis mode is one of the best indicators we have that normal (if slightly different) life is returning.

What does all this tell us about demand for professional services?

Our pandemic recovery path is proving to be the best guide to how ambitious clients are about the future—and this in turn has a direct and material bearing on their expectations around spend on external support. Although 58% of clients who say their organisation continues to be in crisis mode have more ambitious corporate goals than before the crisis, that proportion rises to 77% of those who’ve reached normality. Similarly, 44% of the minority of clients whose ambitions are less than they were before the crisis expect to buy more consulting services over the course of the next 12 months, but among those whose ambitions are now greater than they were pre-pandemic, 68% expect to spend more. Extrapolating this data to the rest of the professional services industry suggests that, as clients feel they’ve reached a state of normality, their expenditure on external support—which is already strong—will continue to grow.

If you are a journalist or work for a news organisation and would like to reference our data, please get in touch with David Pippett at david@proservpr.com