The services clients are most likely to buy during the current period of economic turmoil are…

Three quarters of clients have more ambitious corporate goals than they did prior to the pandemic, and recognise that, against a background of economic turmoil, they’re more dependent on external support than ever. But that doesn’t mean they’ll need the same types of consulting services.

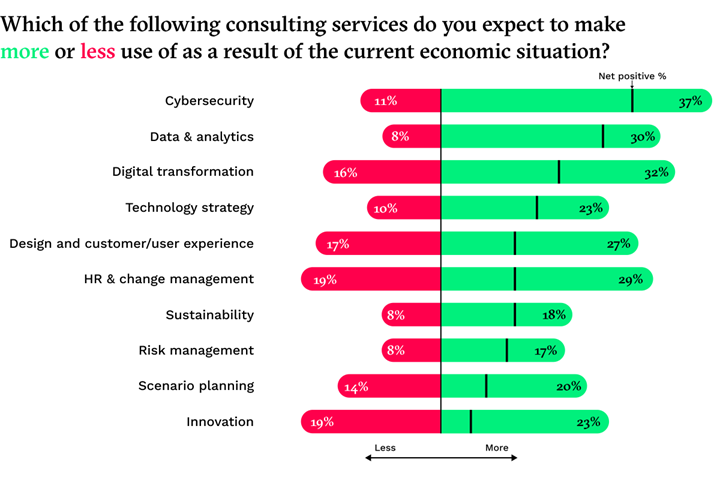

As part of our ongoing research, we regularly ask clients to indicate which consulting services they’re most—and least—likely to buy in the coming months. Recently, we’ve been asking this question specifically in relation to the current trading environment. Putting the resulting responses side by side gives us a sense not just of where clients are likely to focus their consulting budgets (represented by the green bar in the chart below), but also where they’re more likely to try and do the work themselves (represented by the red bar). The higher the net proportion of clients saying they’ll spend more, the greater the potential for growth in the consulting market.

Focusing on the top ten services—those where the net proportion of clients saying they’ll spend more is highest—highlights some important points.

Unsurprisingly, the first is technology. The top five services are wholly or highly technology-dependent; of the next five, only innovation has a strong technology component. Cybersecurity, data & analytics, and digital transformation all headed the list in our Q3 survey, suggesting that demand for these three services is more likely to stay high, while others wax and wane. Of the three, digital transformation is the most susceptible to clients trying to do more of the work themselves, something that’s reinforced by the relatively poor performance of target operating model work (now and three months ago). In this, most recent data, just 6% of clients say they’re most likely to use external help in this area, while 11% say it’s the least likely area. By contrast with digital transformation, cybersecurity and data & analytics have strong net-positive scores of +26% and +22%, indicating that clients completely recognise the need for, and value of, outside help. Technology strategy and design and customer/user experience both appear to be more important than they were three months ago, clearly, being pulled along in the wake of technology-related change.

The data where HR & change management is concerned is more complex in terms of relative importance, but at the same time the net proportion of clients saying they expect to spend more (10%) is higher than it has been in other research we’ve carried out over the last few months. Therefore, what may be emerging here is a more polarised picture, with an increasing number of clients planning to spend more on consulting work in this area, but a significant proportion holding firmly onto the idea that this is the type of work they’re best placed to do themselves. Sustainability continues to hold its ground, despite the prevailing volatility, while risk management and scenario planning continue to play an important role.

Taken in the round, this data suggests a sea-change in the way client organisations deal with crises. In the past, client organisations would have resorted to cost cutting and lay-offs; in the 2008 financial crisis, they added cutting consulting expenditure to that heady cocktail. But after a decade of ever-leaner operations and tighter controls on headcount, the impact of traditional approaches is likely to be limited. Moreover, client leadership teams now have their experience of the pandemic to draw on, in which technology is seen to have won the day. Today, clients are pinning their hopes on technology to see them through this array of crises—and they’re turning to consulting firms to help. One final note of caution, however: Consulting firms really need to deliver.