What are the most resilient services?

Our most recent research has highlighted the extent to which demand for consulting and professional services more broadly is proving resilient, despite the macroeconomic uncertainty. But not all services are proving equally resilient.

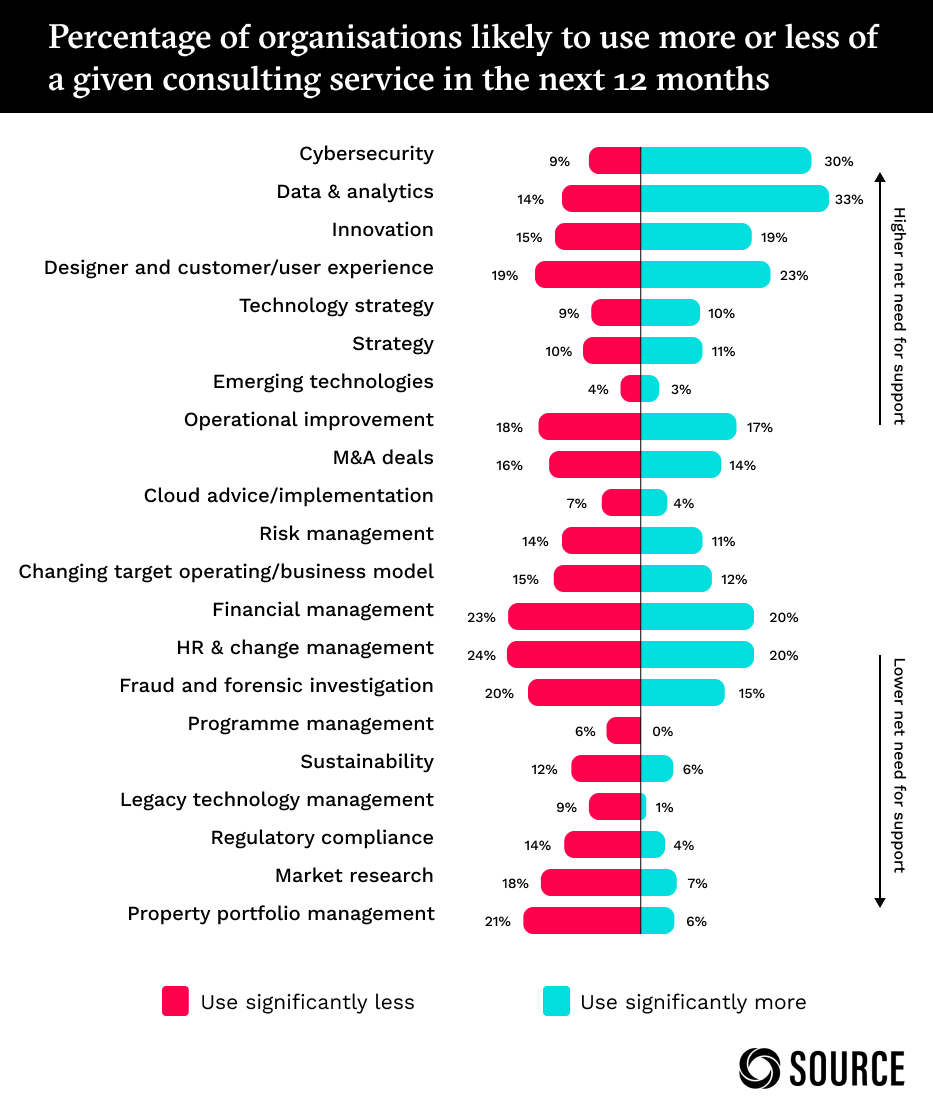

The chart below shows the collective views of around 1,300 clients, gathered over the course of the last six months, about where they’re most and least likely to use external support. Services are ranked in terms of the highest to lowest net positive of these two figures. A high positive score indicates a widespread recognition among clients that they’ll have to make substantial use of external support in this area. A high negative score doesn’t necessarily indicate that clients aren’t investing in this area but suggests that clients will be aiming to use their own, in-house resources to carry out this work. We know, for example, that HR & change management is one of clients’ most important, long-term areas of investment, but it’s also one that clients think they should be able to deal with themselves.

There are some areas where the balance of clients’ opinion is clear. Cybersecurity, the need for which has been boosted by the Russia-Ukraine war, requires significant levels of deep, up-to-date skills, which client organisations are unlikely to have. Only 9% of clients think that this is an area where they’re least likely to use external help, compared to 30% who say they’re most likely to do so. A shortage of skills and the need for increasingly sophisticated tools is also driving demand for data & analytics, but demand here is also being significantly strengthened by the current uncertainties. During the pandemic, one of the biggest lessons for clients was that they didn’t have the right kind of information about their business and operating environment to make informed and fast decisions—and they’re now, again, looking at how effective their ability to keep a finger on the pulse of the market actually is. However, although a third of clients say data & analytics is one of the areas where they’re most likely to be using external support (the highest of any of the services we asked about), 14% say it’s the area where they’re least likely to do so, suggesting that some organisations at least are still trying to build up their own, in-house expertise.

There are several services where clients’ views are more polarised, but perhaps for different reasons. Innovation and design/customer experience haven’t always been so high-up when it comes to clients’ willingness to use external support. That they are now highlights the extent to which economic uncertainty has made clients more focused on pursuing revenue growth, through the launch of new products/services and/or the expansion into new markets. Knowing that it will be difficult to improve productivity, especially if the money available for large-scale technology change may be threatened by rising costs, increasing sales may look like the easier option, but external support will be useful in accelerating the process.

But the polarisation of demand for operational improvement and HR & change management should give professional services firms pause for thought. (Financial management is a relatively small market and largely the preserve of the Big Four, so we’ll discount this.) Many clients believe they’re better placed than external advisers to deliver work around productivity and organisational change, largely because they don’t see consulting and other firms bringing anything new to the table. Both areas have suffered from a chronic lack of investment on the supply side for the last 20 years, creating a vicious circle whereby a lack of innovation has depressed demand, which in turn reduces the incentive among suppliers to invest.

Both productivity improvement and organisational change will be critical to clients’ ability to withstand the current “age of crises”, and they should be among the most resilient of consulting services. The professional services sector has very little time to make good its investment deficit.