Growth options in a challenging market

With no sign of an end to global political and macroeconomic uncertainty, consulting and professional services firms will need to look for growth in new markets and services. They may also need to challenge their own business models.

The latest slowdown in the consulting and professional services industry shows no sign of returning to growth by way of the steep recovery we saw after the global financial crisis in 2008-9 and in the aftermath of the pandemic. Then, client organisations were facing a small number of very clear threats that, as they evaporated, triggered the release of a pent-up desire for change, fuelled by new ways of using technology (digital transformation and AI). Now, clients face multiple, simultaneous challenges: worries that consumer expenditure is weak, but their costs are still rising; concerns that their international markets and operations may be under threat from trade barriers and tariffs; fear that they don’t have the resources to respond.

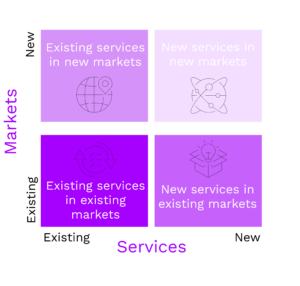

Four strategies for growth

In this environment, consulting and professional services firms can’t rely on their growth coming from continuing to sell their existing services to the markets they know well. Venturing further afield, they should be looking at new services for their existing markets, new markets for their existing services—and, perhaps most dauntingly, launching new services in new markets.

New services for existing markets: Speaking to clients, there’s definitely a sense of fatigue with firms’ typical portfolios of offerings. In a lot of service areas, the proportion of clients we survey who tell us they’re very likely to spend on external support is matched by an almost equal proportion who say they think they can do this work themselves.

Where there is interest is in multidisciplinary services. Digital transformation is the most familiar of these, but clients are looking for multifaceted support in other areas, too: growing their businesses, improving performance, becoming more sustainable, and protecting themselves from threats.

However, developing new services puts pressure on firms to change and invest; it can also confuse clients who don’t know which firm to use for what.

Key multidisciplinary services

Existing services for new markets: Conventional thinking defines markets as geographical or based around specific industries, but there’s an opportunity for firms to explore new markets closer to home.

Our research highlights the extent to which clients’ buying habits are changing. In the past, we might have expected a chief operations officer, for example, to buy operations-related services, but now they’re also buying strategy and technology support. Similarly, a chief HR officer used to almost exclusively buy HR services, but now they’re also buying technology ones. Technology sits in the middle of this web, drawing almost all other functional roles in: More than 60% of chief risk officers buy technology (and strategy) services alongside more traditional risk work.

There are challenges here, too. A firm that’s optimised its go-to-market strategy around the chief financial officer—who, our research suggests, will be more determined to find a firm with deep sector expertise than one that knows how to get things done—may find they’re wrong-footed when selling their services to a COO who prioritises sector expertise and the ability to implement. More fundamentally, the biggest barrier to selling to a new client, even one who’s working in an organisation you know well, is overcoming their past experience of working with other firms.

New services in new markets: Unquestionably the hardest to execute, this option may be the one that offers up the greatest long-term growth potential. The wind is blowing firms right across the consulting and professional services sector to focus more on delivery and less on advice. That’s not new. What is new is that this change comes at a time when many client organisations are rethinking their business models, including which of their activities could now be done more efficiently and, with the help of new technology, better, if given to third parties.

Thirty years ago, a similarly intense debate about what an organisation’s “core” business was resulted in the birth of the outsourcing and then offshoring industries—and something similar could be on the cards again today. Most consulting firms—indeed, most professional services firms—missed out on the opportunity in the 1990s because there was still plenty of growth selling their existing services in their existing markets, thereby opening the door to new suppliers.

Given the challenges in today’s market, consulting firms will be keen not to make the same mistake again.

What can firms do next?

If you would like to understand more about clients’ buying behaviours in the market today and how you can use Source’s market data to identify growth opportunities for your own firm, then do get in touch. Our bespoke leadership briefings can help you reshape your strategy and invest where it matters.